Low interest rates are a cause to rethink conventional wisdom

The Consumer

It comes as no surprise that the historically low level of interest rates has been a tremendous advantage to consumers who want to refinance their mortgages and other loans. Borrowers with high credit scores have had access to cheap money, often obtaining a fixed loan for 30 years for less than 4%! If you can save at least 1% on your current loan by refinancing, it may be time to consider restructuring.

You may also consider not rushing to pay down your mortgage, and instead use the low rates to your advantage and invest the excess dollars elsewhere.

Corporate

In addition to everyday consumers, business owners and managers for small and large organizations also have access to money at rates that have not been available very often. We are in the middle of the COVID-19 pandemic, so many will argue that the low rates are a symptom of the lack of demand that exists for lending; that they really are an indication of expected economic activity in the future. This certainly is a valid point, but low interest rates are not a new phenomenon. We have seen this story before. After the dotcom bubble burst, I remember 0% financing available on certain makes and model of cars. During the Great Recession, the 90-day Treasury Bill went to a negative interest rate temporarily. Post the Recession up to and including as I write this article, we can find negative yields on longer term government bonds such as the German 10-year Bund which sits at approximately -0.40%!

So, who loses given the current interest rate environment? Savers and retirees, primarily. Earning an attractive return while maintaining a low risk profile has proven to be exceedingly difficult. Those who are saving for a short term need or looking to live off the interest that their savings produces, have found that their income has gotten smaller as government and corporate balance sheets have grown exponentially.

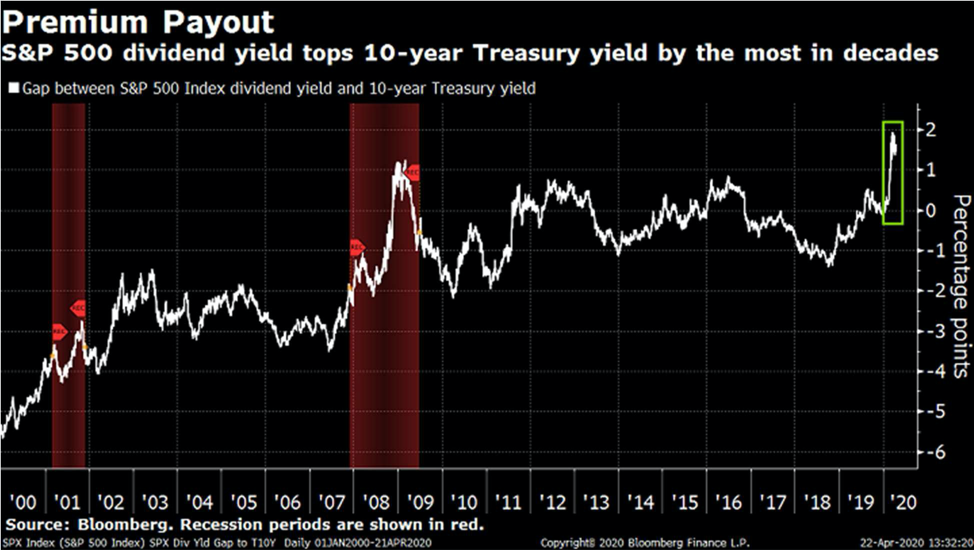

Please observe the chart below which demonstrates the relationship between the dividend yield on the S&P 500 index and the U.S. 10-year Treasury Note:

The red shaded areas are the time periods when we were in recession (2001 and 2007-2009) and the white line represents the difference between the yield on the S&P minus the yield on the 10-year Treasury. For example, if the S&P yield is 1.5% and the 10-year yield is 4%, then the line would plot as -2.5 (1.5 minus 4 = 2.5). The line is now plotting above zero, which as you can see is not a common occurrence. Additionally, the amount above zero is even higher than the level seen during the Great Recession.

What to do?

What does this all mean? In my opinion, we can expect to be a low interest rate environment for the foreseeable future. Therefore, I wouldn’t hold my breath on earning an attractive yield on my savings. The phrase “when life give you lemons, try to make lemonade” is well known, but which lemonade recipe should you use? There are several options, from real estate, hard money loans, dividend paying stocks, and low-grade bonds. No one vehicle is right for all, but it is better to explore your options rather than wait for interest rates to return “normal”.

The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. Prior to making any investment decision, please consult with your financial advisor about your individual situation. Any opinions are those of the author, and not necessarily those of Raymond James.

This article was written by Gus Vega, Certified Financial Planner, Total View Advisors and Branch Manager with RJFS. He can be reached at 786.315.4870, 9155 S. Dadeland Blvd. # 1014, Miami, FL 33156. Total View Advisors is not a registered broker dealer and is independent of Raymond James Financial Services, Inc. Securities offered through Raymond James Financial Services, Inc., member FINRA / SIPC. Investment advisory services offered through Raymond James Financial Services Advisors, Inc.