Federal Reserve chairman’s views are starting to become clearer

Raymond James Chief Economist Eugenio J. Alemán discusses current economic conditions.

For a Federal Reserve (Fed) chairman committed to reducing noise coming from the institution and/or to changing how the Fed communicates, his first attempt to do so was not very promising. Just after Chair Warsh’s first press conference, we argued that inflation was not a choice, as he suggested during the press conference.

But in his first appearance at the Semiannual Monetary Policy Report to the Congress, Chair Warsh hit the right tone. However, some editorials got it completely wrong, as the chairman did not say that inflation will be a “thing of the past,” as some indicated. The nature of the beast, i.e., of inflation, prevents it from ever being a “thing of the past,” so we were immediately concerned that the chairman of the Fed could be saying something like that. But this is not what he said. He never said that inflation will be a “thing of the past.” To say that is to not understand what inflation is.

What the Fed chairman said was: “And if we get policy right – and we will – the inflation surge of the last five years will be a thing of the past.” This response was much better than saying that inflation was a choice. But what he did not say was that, although they have the tools to combat inflation in the future, there would probably be other episodes of high inflation in the future. It is inevitable! Today is a clear example of this.

The Fed cannot control what happens in geopolitics, what happens to oil prices, what happens to federal spending, what happens to supply chains – both domestic as well as global – what happens with plagues, etc.

The Fed cannot keep inflation at the target all the time because life happens. The only thing the Fed can do is to conduct monetary policy to bring inflation back to the target once inflation has deviated from it. Some argue that the Fed was late to increase interest rates as the economy exited the COVID pandemic.

But does the Fed have the power to shorten the period where inflation stays above the target? Yes, but there is always a tradeoff, and sometimes the tradeoff is very costly.

One of the ways to shorten the time that inflation stays above the target could potentially have severe consequences for the economy. Sometimes, if inflation is too high, they may choose to increase interest rates so much that the economy could suffer a potentially severe recession. So, the solution is not so clear cut, but they could ultimately go that route.

Will this Fed chairman take that route? First of all, if he feels that this is needed, he will have to convince many of his colleagues, and that is not a sure thing so early in his tenure. For now, we still believe that interest rates are still somewhat restrictive and that the Fed could wait until there is more clarity on what the spillover effects of higher oil prices are, if any. Therefore, our base case remains that we do not foresee a recession over the next 12 months.

June inflation shows why the Fed should wait for more clarity

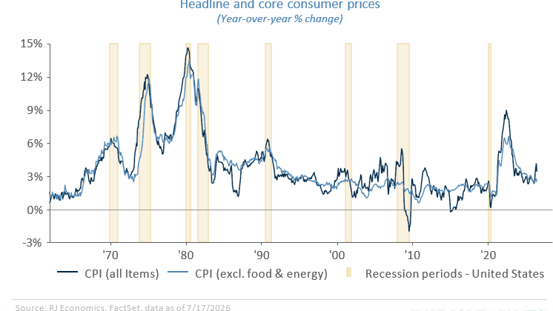

This week we had a very good inflation number: the Consumer Price Index (CPI) for June. Markets were expecting it to be slightly negative, but it came in much lower, at -0.4% month on month, with the year-over-year rate dropping from 4.2% in May to 3.5% in June.

What was not expected was such a weak reading for core CPI, which came in flat compared to expectations for a 0.3% month-on-month increase. Some of this weakness came from the very low 0.1% increase in shelter costs, which represents about 33% of the weight of the CPI. But this weakness was also observed across many sectors of the economy, which could indicate that there is very little space for firms to increase prices.

That is, there was very little indication of higher gasoline prices spilling over to the rest of the economy, which is good news for the Fed and for interest rates during the rest of the year. The not-so-good news is that this was just one month of data. But if the data continues to point to little spillover to the rest of the economy, and we continue to see relatively low month-on-month increases in shelter costs, Fed officials will probably remain on the sidelines for the rest of the year, which is our current call.

Economic and market conditions are subject to change.

Opinions are those of Investment Strategy and not necessarily those of Raymond James and are subject to change without notice. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no assurance any of the trends mentioned will continue or forecasts will occur. Past performance may not be indicative of future results.